SHANGHAI, Feb 10 (SMM) - In 2021, the prices of silicon metal exceeded 10,000 yuan/mt, reaching a maximum of 70,000 yuan/mt fuelled by the supply side. The price trends of silicon metal during the year are roughly divided into three stages:

From January to May, the prices were basically stable.

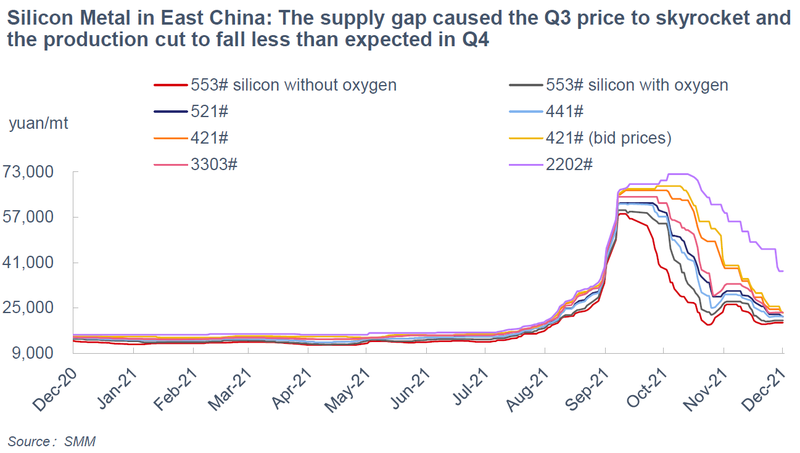

From June to September, the silicon metal prices rose steadily on disruptions to the supply side. In early June, a fire broke out at Hoshine Shihezi silicone plant. The market broadly expected that the company's silicon metal production capacity would be affected and the output would be reduced. Meanwhile, the drought in Yunnan delayed the production resumptions at silicon plants until mid-June. Hence the silicon metal prices rose. In July, the production at silicon plants was inconsistent due to the power rationing in Yunnan. In the latter half of the month, East Hope stopped the production due to an industrial accident.

In August, the shortages of cleaned coal intensified, and the output of #421 silicon in the major chemical-grade silicon producing region - Sichuan - was greatly reduced due to the suspension of coal supply in Ningxia. The expectations over higher supply and lower prices during the wet season did not pay off in 2021. The prices hit a record high as the supply shortages of silicon metal emerged amid the surge of domestic and overseas demand.

In addition, as a number of places failed to complete the goal of dual control of energy consumption in the first half of the year, many silicon metal producing areas such as Xinjiang, Yunnan and Fujian were further restricted in terms of energy consumption. The Yunnan Provincial Development and Reform Commission announced on September 13 that the output of local silicon metal plants from September to December shall not exceed 10% of that in August, which fuelled the market's expectations over supply shortages in the year. In this scenario, the silicon metal prices surged from 20,000 yuan/mt to 40,000 yuan/mt. A week later, the production reduction policy of Dehong Zhou, a main producing area in Yunnan, was introduced. The prices of silicon metal jumped nearly 10,000 yuan/mt or nearly 20% in two consecutive trading days, reaching the 60,000 yuan/mt level.

From October to December, the output cuts driven by the dual control of energy consumption were less than expected, and the demand weakened at loss-making downstream producers. After the silicon metal prices surged in late September, the market transaction volume fell significantly. Some aluminium alloy plants suffered from losses for more than a month. After the silicon metal prices peaked at 60,000 yuan/mt, the silicone sector also suffered cash flow issues.

Before the National Day holidays, some traders took profits and sold off their cargoes. Some aluminium alloy factories that had stopped the production began to liquidate the silicon metal inventory. Silicon metal plants in Yunnan resumed the operation after the National Day holidays, and the expectations of output cuts amid the dual control of energy consumption failed to pay off, which grew the market pessimism and triggered selloffs. Meanwhile, the productivity of aluminium alloy and polysilicon slid due to the power rationing. Silicone monomer plants cut the output and lower their prices due to the falling orders and high inventories of finished products. The downstream buyers purchased on demand and lowered the raw material inventory amid market pessimism.

At the end of November, the mainstream prices of silicon metal dropped to 20,000-30,000 yuan/mt. But there were still huge profits for the enterprises that produced high-grade silicon metal. The silicon metal plants in south-west China could proceed the production with electricity from the power grid, hence delayed the output cuts during the dry season. The silicon metal prices continued to fall until mid-December. By the end of December, the price difference between silicon metal with similar quality narrowed to less than 1,000 yuan/mt, and the selling prices of some specifications were close to the production costs of high-cost capacity. As such, the declines in silicon metal prices slowed down.

Growing demand will drive the growth in silicon metal supply, producers will reap high profits during the period of supply deficit

Will the high prices of silicon metal in 2021 extend into 2022? The core variable is on the supply side. Under the optimistic forecast (the dual energy consumption control policy still in place and the reduction in power supply in Yunnan during the dry season): In the first half of 2022, the operating rates will remain low in south-west China, and the consumption will recover in February-March due to the seasonal factor, which will allow the market to enter a cyclical destocking period, and the prices are expected to rise. The release of new silicone and polysilicon capacity will boost the demand for silicon metal in the first half of the year. At the end of the destocking cycle, that is, the beginning of the rainy season in south-west China in June-July, the prices of silicon metal are expected to reach the peak of the year. The commissioning of new silicon metal projects in Xinjiang and Yunnan, together with lower costs during the rainy season, will weigh on the prices of silicon metal.

Under the optimistic forecast, the price range of #553 silicon will be 16,000-25,000 yuan/mt, and the price range of #421 silicon will be 20,000-30,000 yuan/mt. Under the pessimistic forecast (relaxed energy consumption dual control policy and sufficient power supply during the dry season in Yunnan), the impact of the seasonal factor will disappear, the operating rates in the industry will depend on the changes in profits. In Q1 2022, the prices will drop below the costs, which will lead to suspension of production. Considering the time required for the restart of silicon metal capacity and the marginal change in demand, the price peak of the year is expected to appear in April-May or June-July. In the second half of the year, the average cost in the industry will decline after the arrival of the rainy season, and the prices of silicon metal will touch the bottom of the year in November when the supply peaks.

Under the pessimistic forecast, the price range of #553 silicon will be 16,000-22,000 yuan/mt, and the price range of #421 silicon will be 18,000-25,000 yuan/mt.

The expansion of silicon metal capacity will be mainly driven by growing demand from the silicone and polysilicon sectors. However, the high profits are unlikely to sustain amid the excess capacity and low value-added of products. In the long run, the centre of the price range will be 17,000-22,000 yuan/mt.

To access full SMM China Silicon Industry Chain Annual Report 2021-2025, please contact Michael Jiang at michaeljiang@smm.cn or T: +86-21-51666812 |M:+86-1522-1415-920.